As tech has grown, policy debates have become an important pastime. Today’s tech industry aspires to replace human drivers with self-driving cars, secretaries with AI assistants, permanent jobs with gigs — and as a result, the human impact of tech has become an everyday conversation.

No other idea is as emblematic of this as Universal Basic Income, a policy that would distribute a monthly sum to every adult regardless of their income or employment status.

The conversation is widespread. Mark Zuckerberg and Elon Musk have said that UBI may be desirable or necessary. Y-Combinator Research and Facebook co-founder Chris Hughes are running basic income studies. Tech-friendly presidential hopefuls Bernie Sanders and Andrew Yang support the issue.

But should the average tech entrepreneur or investor support UBI? The answer is not entirely clear.

The good news is that the tech industry is deeply familiar with risk, which is an important component of arguments for UBI. The bad news: risk isn’t the whole story, and both positive and negative evidence for the policy are currently thin.

Image via H. Armstrong Roberts/ClassicStock/Getty Images

The role of risk

Entrepreneurs understand the risk component of UBI because it’s the same risk they take in starting companies. Many entrepreneurs start with savings or seed funding that reduce their downside risk — and it’s not hard for them to imagine that others lack these resources. A UBI could solve the issue.

“The hypothesis is, [UBI will] fundamentally change people’s lives. They’ll do something different from what they were doing, because they have a continuous stream of basic income they can depend on. They can start small firms, invest in assets that give them better incomes and wealth, and that translates into better health and education for their kids,” summarizes Tavneet Suri, an applied economics professor at MIT who is helping GiveDirectly run a UBI program providing about 75 cents per day to recipients in rural Kenya.

Risk is clearly important in the developing world, but it’s also an increasingly urgent story in the US. Rates of new business formation have, in recent years, fallen below business closings. There’s a correlation between low entrepreneurship and low savings rates: 40 percent of American adults say they can’t cover a $400 emergency expense, according to the Federal Reserve. Starting businesses may simply be too risky for this generation.

In fact, a newly insecure class is already growing in developed countries worldwide. Guy Standing, a professorial research associate at the University of London, calls this class the precariat. “What is distinctive about global capitalism today, and this will continue, is that even many of those currently earning enough to put them into middle-income categories feel insecure, and often live on the edge of unsustainable debt,” Standing wrote to TechCrunch. “What is significant for those interested in promoting entrepreneurial risk-taking is that one can show that the emancipatory value of a basic income is greater than its monetary value, which is the opposite to all other forms of social policy.”

The universality of risk in both rich and poor countries is a positive for UBI proponents, since studies like Suri’s are taking place in the developing world. An argument can easily be made that behaviors like immigrating to a city or going to college may be riskier in developing countries, but also carry risks in the rich world, which aren’t necessarily offset by financial instruments like loans. “I would never have done my Ph.D. if I’d had to pay for it. There’s no probability in any world. I wouldn’t have wanted to take the loans, because what if I don’t get a job?” says Suri.

However, it will take years to answer the question of how UBI interplays with risk. Suri’s study, for instance, includes cohorts who receive an up-front lump sum, a 2-year monthly UBI payout, and a 12-year payout — so the full effects won’t be visible for some time.

Image via Getty Images / iNueng

The effects on workers

Estimating the effects of a UBI on entrepreneurship, immigration or higher education offer clear arguments for risk. But when it’s extended to people who are currently employed and have no obvious need or desire to start their own company, the picture becomes more muddled.

Some hypothesize that a UBI could lead to workers quitting jobs, or the unemployed choosing to stay that way. Wesley Pech, a behavioral economist at Wofford College, frames these possibilities as a tension between two theories of consumer behavior. The income effect and substitution effect respectively predict that people given basic incomes would choose unemployment or choose to continue seeking work. No basic income study has definitively shown that either outweighs the other. “I can’t think of an experiment so well designed that it could serve as a benchmark,” says Pech.

So here, too, UBI needs more study. But for the time being, anecdotal reports praise basic income.

In Germany, which is generally regarded as fairly wealthy and egalitarian, a startup called Mein Grundeinkommen is using crowdfunding to supply a €1,000 monthly income to 316 people, and currently adds about 15 more people each month. Founder Michael Bohmeyer says universality is an important psychological component of basic income.

“When you frame basic income as a poverty distinction instrument, then it feels like welfare money. You’re the one who didn’t make it, the stupid one, and now you get money to fix it,” he told TechCrunch. “Basic income is something else, it’s for everyone and free of conditions.” That leads to different results than welfare. For instance, one older man on welfare — an identical amount to the Mein Grundeinkommen basic income — decided to end his own unemployment by starting an online business after receiving his basic income from Mein Grundeinkommen.

The psychological effects can be huge even for the well-off. “Surprisingly, we’ve found out that the people who thought that they wouldn’t really need it, they had the biggest effects and changes in their lives,” says Bohmeyer.

Image via Getty Images / Mongkol Chuewong

Another of Mein Grundeinkommen’s basic income recipients was unhappy with her family inheritance, a hotel she was expected to run. After starting to receive her stipend, she had the mental space needed to work through her issues, and took the steps necessary to become a good business owner.

“We have a strong idea that when basic income is introduced, people will stop working. This is even what people think before receiving the money. They think, I’ll start a business, I’ll quit my job, and we have a lot of women who say, I’ll quit my marriage to my stupid husband because I’m not dependent on him anymore. All of a sudden, the basic income comes, and you have more possibilities. You’re free to go. Once you can say no, it’s different to say yes,” says Bohmeyer.

These stories reveal a side of UBI that goes beyond risk and basic human behavior: it can also be framed as an argument for basic human dignity, and a world that exists for more than just work. “The people with basic incomes seemed to not be so ego focused anymore, they had an empathetic, wider approach to look at the world,” says Bohmeyer.

“It sounds so silly when I say it, but that’s what I realized. I think we need to find more about this because we have tremendous changes in our society. It’s the ending of the industrial age and beginning of the digital age, and I think this is what we need in our society.”

At the end of the day, though, Mein Grundeinkommen’s stories remain anecdotal, and thus flawed, just like past basic income studies. Bohmeyer is aware of the problem: Mein Grundeinkommen will join the ranks of more rigorous projects by the end of this year, as it works with the German government to begin a multi-year study giving €1,200 monthly to on 100 participants.

And that’s the best policy that anyone in tech can take: wait, watch, and if possible, contribute support to the studies taking place around the world. UBI is too complicated an issue for partisan stands or knee-jerk reactions. And in the future that the tech industry expects and hopes for, it may yet prove to be one of the best policy ideas available.

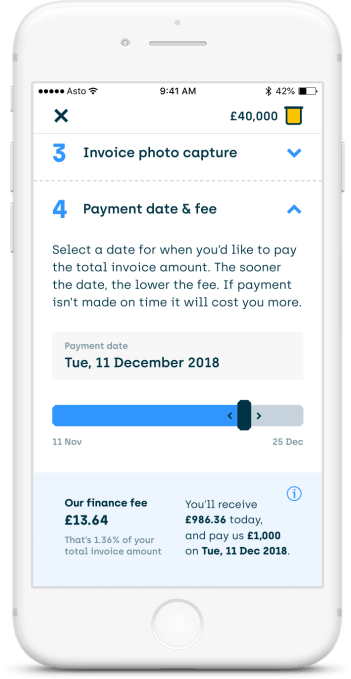

In a demo I’m given of the new invoice financing feature, it all feels relatively painless. After signing up to Asto and applying for the micro-finance option, you’re given an estimated pot of credit from which to drawn down on per invoice financed.

In a demo I’m given of the new invoice financing feature, it all feels relatively painless. After signing up to Asto and applying for the micro-finance option, you’re given an estimated pot of credit from which to drawn down on per invoice financed.